CBAM - Questions and Answers

What is CBAM?

The EU CBAM (Carbon Border Adjustment Mechanism) is an EU regulatory system designed to price the embedded carbon emissions in products imported into the EU. Its purpose is to create a level playing field between EU-produced goods which are subject to carbon pricing under the EU Emissions Trading System (EU ETS) and imported products from countries without equivalent carbon pricing regimes.

Under CBAM, importers must monitor and report emissions associated with the production of certain goods (including iron and steel, cement, aluminum, fertilizers, electricity, and hydrogen) and purchase CBAM certificates corresponding to the amount of greenhouse gas emissions embedded in those products. This financial adjustment mirrors the carbon costs that would have been paid if the goods had been produced within the EU. Find the European CBAM Legislation and Guidance here.

Is CBAM a tax?

No. CBAM is not a tax or a customs duty.

It is a regulatory mechanism that mirrors EU carbon pricing and is directly linked to the carbon footprint of a product.

What does CBAM mean from a sales perspective?

CBAM puts a carbon cost on imported goods entering the EU that mirrors the EU Emissions Trading System (EU ETS). For cases where standard quantities can be supplied from stock, the sales price will include CBAM. For mills whose emissions data are unknown or not verified, larger volumes may give rise to pricing uncertainty of such magnitude that supply can only be offered on the basis of subsequent pass-through of the CBAM costs.

To minimize these risks of our customers, Arcus is committed to building strong business relationships with selected manufacturers, who also understand and support a sustainable business.

What does it mean from a procurement perspective?

CBAM introduces cost differences between suppliers based on emissions. Suppliers that work actively on reducing the carbon footprint along the supply chain will be more competitive. Once the emission data of the mills and their suppliers are verified by the EU accredited verification bodies, carbon emissions become a measurable and comparable factor in purchasing decisions.

Can CBAM be avoided?

No. CBAM applies to all covered imports into the EU.

However, the CBAM costs can be reduced by sourcing from producers with lower carbon emissions and reliable, verified emissions data.

Why is CBAM being introduced?

The Carbon Border Adjustment Mechanism (CBAM) is the EU's tool to put a fair price on carbon emitted during the production of carbon-intensive goods that are entering the EU, and to encourage cleaner industrial production in non-EU countries. It ensures imported goods face a carbon price comparable to domestic products, protecting local industries, incentivizing global decarbonization, and supporting EU's net-zero goals .

Which products are affected?

CBAM applies to high-emission goods imported into the EU, including cement, aluminum, fertilizers, hydrogen, electricity, and iron and steel products falling under covered CN codes such as:

Tubes and pipes;

Flanges;

Fittings;

Industrial components

CBAM applies regardless of end use (industrial, construction, consumer). For stainless steel, this means that the CO₂ emissions associated with production, including certain pre-processed materials, must be reported and covered through CBAM certificates.

Why does CBAM matter for stainless steel?

Stainless steel is energy- and emission- intensive due to:

Electric arc furnace (EAF) electricity consumption;

Alloying elements (nickel, chromium, molybdenum);

Upstream ferroalloy production.

Producers outside the EU often operate without explicit carbon pricing, making CBAM directly relevant for imported stainless steel products. Without CBAM, EU mills would face higher costs than non-EU producers. CBAM protects EU mills and forces import prices to reflect the carbon footprint of an imported good; it makes emissions transparent as a commercial factor.

When does CBAM affect imports financially?

Since 1. January 2026, CBAM moved from reporting only to financial obligation. Importers must purchase and surrender CBAM certificates that reflect the embedded carbon emissions of the imported goods. Market prices for goods under CBAM regulation are the refore expected to increase in 2026.

How does CBAM work in practice?

The EU’s CBAM has been phased in over several years. From October 2023 to the end of 2025, importers reported on embedded emissions as part of a transitional phase. From 1 January 2026, the mechanism entered its definitive regime, and importers now have the following duties:

They must be authorized as CBAM declarants before importing goods covered by CBAM regulation;

They must calculate embedded carbon emissions for each shipment either with the producer’s effective emissions or by applying default values;

They must purchase and surrender CBAM certificates that correspond to the embedded carbon emission of each product imported into the EU;

Annual declarations of emissions are mandatory and must follow specific reporting deadlines and compliance.

Who is responsible for CBAM compliance?

The EU importer of record is legally responsible for CBAM compliance. As a trader, we manage these obligations for the products we import.

What does CBAM mean for the stainless steel industry?

CBAM directly affects iron and steel, including stainless steel products, as they are among the categories covered by the mechanism. The following implications are particularly relevant:

Embedded emissions now carry a financial cost, which may increase the effective import price of stainless-steel products;

Importers’ suppliers must track, document, and get verified for the importer to be able to use their emissions data monitored at the production level. This increases administrative work and requires close collaboration with overseas producers;

Customers will increasingly favor suppliers with low carbon emission to minimize CBAM liabilities;

Companies with lower emissions profiles will gain a market advantage in the EU. Conversely, suppliers without robust emissions data may face cost disadvantages.

How does CBAM affect pricing?

CBAM introduces an additional cost that is linked to carbon emissions coming from the production of a product and/or its precursors. CBAM-related costs reflect transparently if a producer actively works on reducing its carbon emissions during production. Products with higher embedded emissions will become more expensive while lower emission production routes will be more competitive.

When does CBAM affect pricing?

CBAM requires importers to pay for the carbon emissions embedded in their products starting on 1. January 2026. They must buy CBAM certificates, which is expected to add significant extra costs to stainless steel products.

The full financial impact remains uncertain due to:

A complicated methodology to calculate supplier specific benchmarks

Delays in EU accreditation of verification bodies

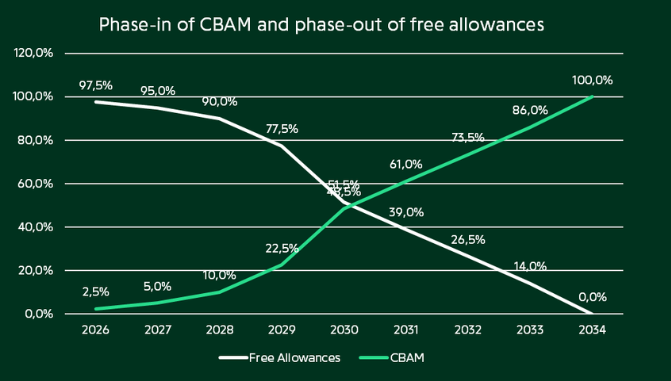

As a result, most importers will likely need to calculate 2026 CBAM costs using country-specific default values. Pricing will be more and more impacted by CBAM over the years as shown in the chart below. Free allowances are emissions permits that certain companies receive at no cost under the EU Emissions Trading System (ETS). They allow the EU companies to emit a certain amount of carbon emissions without buying carbon credits. The free allowance will phase out while the CBAM cost will increase starting with 2.5% in 2026 up to 100% in 2034.

What is the price of a CBAM certificate?

To ensure comparability with EU domestic carbon costs, the price of CBAM certificates is linked to the EU ETS carbon price, which fluctuates based on market conditions. As a result, CBAM costs will vary over time.

On what depend the CBAM costs on?

CBAM costs are transparent and regulation driven. They depend on carbon emissions per ton imported material and the EU ETS price. If for example 2.5t CO₂ / t stainless steel are produced and the ETS price is €80 / t CO₂ the CBAM cost would be €200 / t imported material.

The EU ETS certificates are traded, and the price is volatile and effective CBAM costs are thus difficult to predict now.

Which producers are affected?

CBAM is an EU regulation. All non-EU producers that are directly or indirectly exporting to the EU, must provide verified emissions data to their customers to allow the customer to use the producer’s actual emissions data in the CBAM calculation. If the producer is unable to provide this data, the importer will need to use country specific default emission data instead. These are set high to be punitive. Producers with verified emission data, energy-efficient production and decarbonization strategies are better positioned under CBAM.

Limited emissions tracking, no prior carbon pricing and inconsistent verification standards will lead to higher emissions and higher CBAM cost for the importer.

Can CBAM costs be reduced or offset?

If a producer has already paid a comparable carbon price in the country of origin, this may be deducted from the CBAM obligation. In some cases, importers may offset the cost if an equivalent carbon charge is already paid in the exporting country. As of January 2026, no exporting country complies with the EU rules to qualify for cost offset.

What is the timeline of CBAM reporting?

2026: First regular reporting year. Importers must record the embedded CO₂ emissions of imported products.

2027: CBAM certificates must be purchased for the emissions of 2026. The CBAM report for 2026 is due on 30. September 2027. Importers need to submit the report and surrender CBAM certificates purchased to cover their imports. If verified supplier specific data has been used in the report, all documentation needs to be submitted at the same time. It is unlikely that that all producers (ca. 40’000 globally) will be verified until September 2027, default values may therefore be used to calculate emissions.

Where does verified emissions data come from?

Producers must provide verified carbon emission data to importers for each product imported into the EU. To obtain verified emission data, a third-party auditor accredited by the EU for CBAM purposes (known as a verification body) must conduct a verification audit. For complex products such as stainless steel, the emissions from precursor production must also be verified.

What are the default values for?

If a producer was not audited by an EU accredited verification body and is therefore not able provide verified, product-specific emission data, the importer has to calculate the CBAM cost with the default values that are set by the EU for each CN code and country. Using default values will result in higher CBAM costs to encourage producers to reduce their carbon footprint. Reducing the carbon footprint will give producers a competitive advantage in EU market.

How are emissions calculated?

The emissions relevant in CBAM are direct emissions from the steel production processes (melting, casting, rolling, etc.) and, in some cases, indirect emissions such as electricity.

Therefore, two visually identical product scan have very different CBAM costs depending on the energy mix used in manufacturing, technology, scrap ratio and so on.

What if a non-EU producer has lower emissions than an EU producer?

To ensure fair treatment of efficient non-EU producers, CBAM uses benchmark values. A benchmark is a product-specific reference point representing the emissions of the cleanest EU producers in each sector. This means non-EU producers with lower emissions than the EU benchmark pay reduced CBAM costs or potentially no costs at all, while those with higher emissions pay proportionally more.

What is the role of Arcus in CBAM?

Arcus obtained the status of authorized CBAM declarant in 2025. This means that we can submit CBAM reports independently and provide our customers with verified and transparent support in complying with the CBAM regulations.

As your trusted partner in stainless steel trading, we are fully engaged with the new regulatory requirements. We are working to:

Ensure full compliance with reporting, emissions verification, and certificate surrender obligations;

Collaborate proactively with our suppliers to obtain reliable emissions data and identify opportunities to reduce carbon intensity;

Provide you with up-to-date guidance and support to help you manage CBAM-related impacts on pricing, compliance, and supply chain planning.

We continuously monitor developments and communicate relevant regulatory changes that affect our industry.

What are the long-term implications of CBAM?

CBAM is a structural market change. It will:

Reward low-carbon production routes;

Improve emissions transparency along supply chains;

Increase the importance of ESG credentials;

Influence sourcing strategies and decisions;

Make emissions a commercial KPI and not just a sustainability metric;

Lead to investment in cleaner technologies.

Will CBAM replace EU safeguard quotas or duties?

No. CBAM is not a customs duty or a tariff. It is a climate mechanism that operates separately from trade defense measures. CBAM and the new quota system are separate, but in practice they work together by affecting cost structures, supply chain planning, and sourcing strategies.

Do you have further questions, or would you like to discuss the possible impact on your situation?

Please contact your Arcus contact person.

We are of course at your service.